Your home equity may be more powerful than you realize. If you’ve owned your home for years, chances are you’ve built significant value. That equity could help a younger family member finally achieve homeownership.

At a time when first-time homebuyers are struggling with upfront costs, many homeowners are discovering that using their equity strategically can open doors for the next generation.

For a lot of parents or grandparents, watching a family member struggle to buy their first home right now is hard. That’s because you saw firsthand how homeownership gave your life more stability and helped grow your net worth. You want your loved ones to have those same opportunities.

But with all the affordability challenges in recent years, that can feel like an uphill battle. Fortunately, it’s slowly improving lately.

Here’s what you may not realize. You may be in a unique position to help (thanks to the equity in your current house).

The Equity Advantage You May Not Be Thinking About

You’ve likely owned your home for years, maybe even decades. And during that time, two things happened:

- Home values rose

- Your mortgage balance shrank (or you paid it off entirely)

That combination has created substantial equity for many homeowners like you.

And while you may think of that equity as something you want to have in your pocket for retirement, it can also serve another purpose. It can help the next generation clear the biggest hurdle in their way.

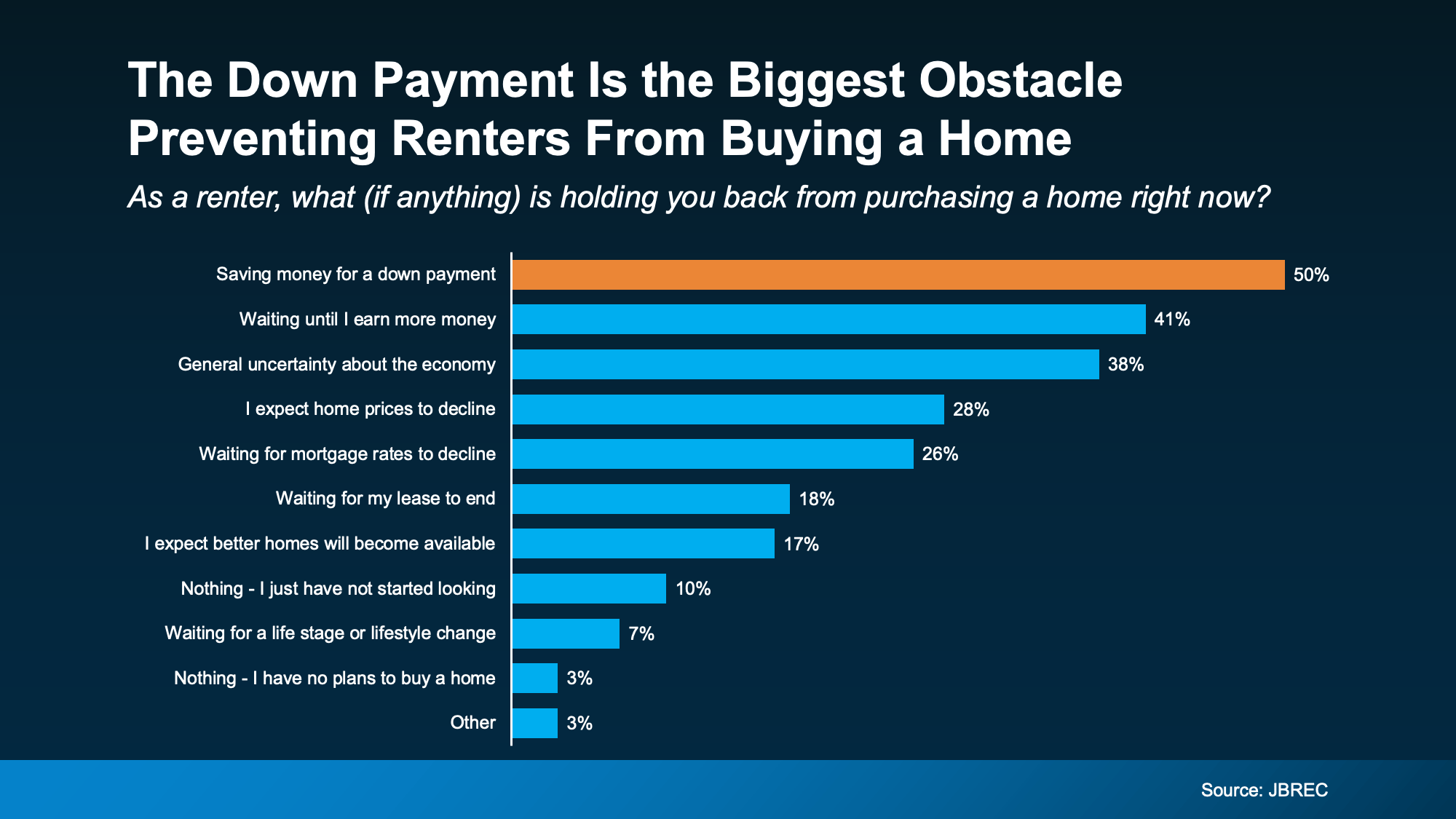

The #1 Thing Holding Young Buyers Back

When John Burns Research & Consulting (JBREC) asked renters what’s keeping them from buying, the top answer wasn’t mortgage rates or home prices. It was the upfront cost, particularly saving enough for their down payment (see graph below):

That’s where you may be able to make more of a difference than you realize. You can’t control rates or prices. But you may be able to use your equity to help with this upfront expense. And giving money to your loved one so they buy a home doesn’t mean putting your own future at risk.

That’s where you may be able to make more of a difference than you realize. You can’t control rates or prices. But you may be able to use your equity to help with this upfront expense. And giving money to your loved one so they buy a home doesn’t mean putting your own future at risk.

Even a small portion of your equity can put them in a position to finally get the keys to their first place – and, if you’re strategic about it, you’d still have a lot leftover for when you retire.

With an estimated $68 and $84 trillion of wealth expected to transfer from older generations to younger ones over the next two decades, many families are already thinking differently about when and how that wealth will be passed down. Maybe it makes sense for your family to think about it too.

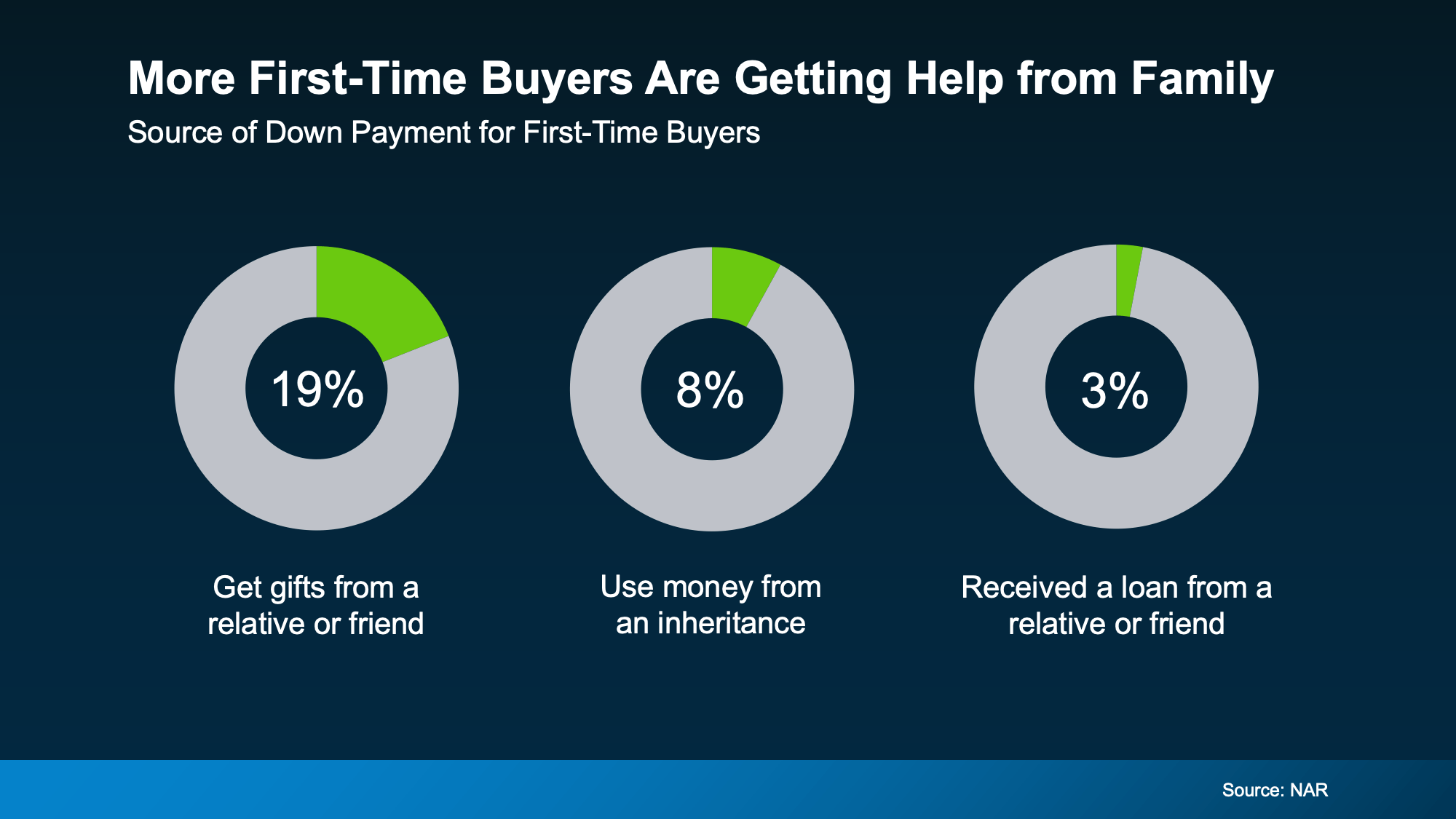

Help from Loved Ones Is Making a Move Possible for Many First-Time Buyers

A growing share of young buyers is using gifts and loans from their loved ones to springboard into homeownership. According to the National Association of Realtors (NAR), nearly 1 in 5 first-time buyers use a cash gift from their family or loved ones for their down payment.

And other young buyers are using their inheritance or a loan from someone they know to finally break into the market (see charts below):

This Is About Opportunity, Not Obligation

This Is About Opportunity, Not Obligation

Every family’s situation is different, and your decision should be made carefully. It’s just that, if you’ve built up a lot of equity, you may have more room to help than you think.

It’s not just a financial gift. It’s giving stability, security, and a foundation that could change their lives for the better – especially at a time when they may not be able to do it on their own.

See What Your Home Equity Can Make Possible

If you’ve built substantial home equity, you may have more flexibility than you think — whether that means supporting a loved one buying a home or making a move of your own.

Before making any decisions, talk with experienced real estate agents who understand current market conditions and equity trends. The right guidance can help you protect your future while creating opportunities for the next generation.

If you’re curious what your equity looks like in today’s market, let’s start with a conversation.

Looking for expert guidance? As a leading Real Estate Agency in Chicago, KM Realty Group LLC helps buyers and sellers navigate the local market with ease. Contact us today for a free consultation.